Conventional wisdom that business property taxes in Minnesota are higher than residential taxes is correct. Residential property taxes are lowered—and business property taxes are raised—through Minnesota’s property classification system, homestead market value exclusion, and other factors, according to an MREA commissioned analysis released today.

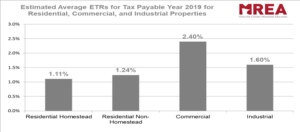

All things considered, the average 2019 commercial effective tax rate (ETR) is about double that of the residential properties, while the industrial ETR is about 40 percent higher, according to the issue report, Minnesota Business Property Taxes: Where We Are, How We Got There.

Approach

Two approaches to examining Minnesota business property taxes relative to other states are examined in this report.

- The first—the 50-State Property Tax Comparison Study from the Minnesota Center for Fiscal Excellence (MCFE)—indicates that business property taxes in Minnesota are generally high relative to other states.

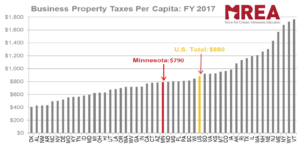

- The second—a comparison of business property taxes per capita and per private sector employee calculated using data from the annual Ernst & Young (EY) business tax report—indicates that they are low.

-

There is a lot of sensitivity on these rankings. Both approaches have shortcomings and neither should be viewed as the final word in Minnesota business property taxes relative to other states.

Key Findings

The gap in Minnesota between business ETRs and residential ETRs has shrunk since 2000—and especially since 2002. Expressed another way, the degree of preferential tax treatment enjoyed by residential properties relative to business properties has declined.

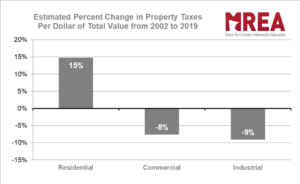

From 2002 to 2019, residential property taxes per dollar of total value increased by 15 percent, while commercial property taxes fell by 8 percent and industrial property taxes fell by 9 percent.

The reasons for this include:

- Increased dependence on referendum market value levies, driven largely by a decline in real (i.e., inflation-adjusted) per pupil state aid to school districts.

- Large business class rate reductions enacted in 2001.

- Caps on growth in the state business property tax.

- The phase-out feature of the homestead market value credit (HMVC) and—later—the homestead market value exclusion.

Preferential Treatment

Lower ETRs for residential properties vis-à-vis businesses has been justified on the basis that housing is a necessity and thus the cost of housing should be reduced through preferential tax treatment, just as groceries are exempted from the sales tax.

Another argument for preferential homestead tax treatment is that homeownership is associated with positive social outcomes, such as increased civic engagement, more stable neighborhoods, improved academic performance among children, and greater financial security.

Furthermore, business properties often consume more public services per dollar of market value (e.g., increased traffic associated with retail businesses) or are associated with other negative externalities (e.g., noise or pollution associated with some industries) and thus should pay a higher ETR.

The findings presented in the full guide do not point toward any single goal or objective. However, this empirically based perspective regarding the current level of business property taxes and the examination of the forces behind trends in business property taxes relative to other classes of property will hopefully contribute to a more informed debate over proposed changes to Minnesota’s property tax system.