The 2019 Legislative Special Session made three property tax changes that impact school finances. Minnesota school district leaders should take a careful look at the implications of these property tax changes now to assess an opportunity to ask for increased local operating revenue support or for a needed facility bond through a referendum Nov. 5. They would need call for the referendum by Aug. 23.

State funding for schools has not kept up with inflation and many schools in the state operate in aging and outdated facilities.

Conditions to Consider

There is some concern that the state’s budget outlook will continue to decline, especially as we head into the next major budget session in 2021. There’s a unique combination of economic and state conditions at play:

- 2017 tax cut bill in Minnesota

- Use of $500 million from the state’s budget reserves for future spending in the recently adopted budget plan

- Continued use of general fund revenue for transportation

- Protracted trade war

- Difficult farm economy and slowing GDP could reduce the revenue available to future legislatures to provide inflationary funding increases for education

Property Tax Changes

Board Authorized Operating Referendum

In the most recent session, lawmakers made a technical cleanup of the confusingly titled $300 Board Authorized Operating Referendum. It now has been rolled into Local Operating Revenue (LOR) and eliminated as a separate category.

There are two tiers of equalization in LOR to maintain no change in the revenue or the state aid for school districts. LOR can be set by the School Board up to $724 per adjust pupil unit (APU). With this change, operating referendums reduced to $300.

The two changes with implications on school district finances are increases in the state share of the operating referendum revenue and the Ag Bond Credit for Bonded Debt levies.

State Share of Operating Referendum Revenue

The new Tier 1 equalizing factor of Operating Referendum Revenue will increase 11 percent from $510,000 to $567,000 for Pay ’20 and FY ‘21. This affects Operating Referendums up to $460 per APU. This is the former $300 to $760 range.

About 83 percent (or 232) Greater Minnesota school districts now qualify for this equalization, an increase of 16 districts (6 percent). Currently, 167 of these 232 have voter approved referendums and will see tax reductions.

The median reduction will be 7.2 percent, with decreases ranging from -0.2 percent to -10.0 percent. This represents a total reduction of $9.4 million statewide. The state referendum aid to replace this reduction totals $10 million, which includes charter referendum aid.

Even more significant is that 102 Greater Minnesota school districts now can ask voters for between $80 and $460 per pupil in operating referendum revenue with a state share. This is because they are not at the maximum allowable $460 per APU in Operating Referendum once $300 is moved to LOR.

An additional 122 school districts with operating referendums above $460 will see a reduction up to nearly 10% in their Pay ’20 operating levy. While some reductions are not large, it may be sufficient to ask voters to use this savings to increase the allowance per pupil and provide needed revenue to educate your community’s children.

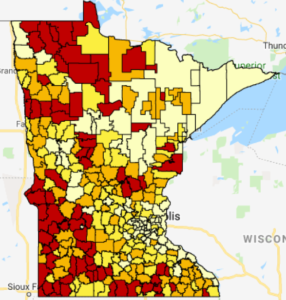

Map >> State Share of Operating Referendum Revenue

The map to the right shows the state share of operating referendum revenue up to $460 per APU with $567,000 Equalizing Factor.

Those school districts highlighted in red will see the highest state share. School districts in orange fall above the state median.

View impact by school district of the state share of Tier 1 voter approved operating referendum revenue

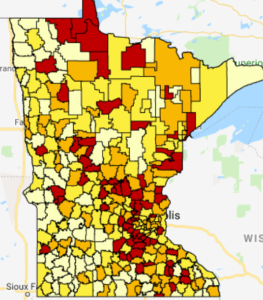

Map >>District Wealth by Referendum Market Value (RMV) per Resident Pupil Unit (RPU)

Map >>District Wealth by Referendum Market Value (RMV) per Resident Pupil Unit (RPU)

The map to left illustrates district wealth across Minnesota as measured by Referendum Market Value (RMV) per Resident Pupil Unit (RPU).

Those school districts highlighted in the lightest yellow have the highest Referendum Market Value per Resident Pupil Unit. Those in the darker yellow exceed in the state median. School districts shown in red have the lowest Referendum Market Value per Resident Pupil Unit. Those in orange fall below the state median.

Ag2School Ag Bond Credit

The Ag2School bond credit will increase from 40 percent to 50 percent in 2020 Pay. This will reduce bonded debt taxes for holders of agriculture and timber land in 296 school districts.

The median reduction per district is $26,568 and $35 per $500,000 in agriculture or timber land. The increased reduction totals $10.9 million.

At 50 percent A2School tax credit, the state share of school bonded debt totals $51.9 million. The median credit per $500,000 in value is $175. This impacts all existing Fund 7 debt levies, with the exception of OPEB bonds.

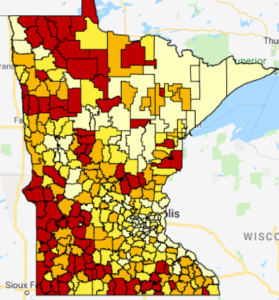

Map >> Ag2School 50% Bond Credit

The map to the right shows the impact of the new 50 percent Ag2School bond credit for farmers and timber land owners per $500,000 in land. This will take effect in 2020.

School districts highlighted in red will see the greatest impact. Those colored in orange also exceed the median credit.

View impact by school district of the change and 50% credit effect on $500,000 in agriculture or timber land value.

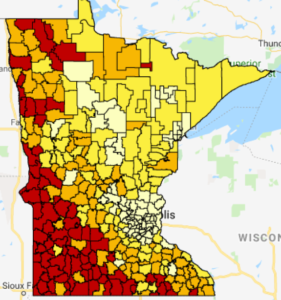

Map >> Agriculture & Timber Land as Percentage of Total Net Tax Capacity

Map >> Agriculture & Timber Land as Percentage of Total Net Tax Capacity

The map to the left illustrates the agriculture and timber land in Minnesota as percentage of total Net Tax Capacity (NTC) by school district.

The school districts highlighted in red will see the greatest impact. Those in orange exceed the median credit. Districts highlighted in the lightest yellow will receive the lowest credit or may not be impacted by the change.

Ag2School Phases to 70%

The Ag2School tax credit on school bonds will increase to 70 percent over the three years. This is permanent law enacted through the tax bill by the Minnesota Legislature.

| Taxes Payable Year | Percent Increase in Ag2School | Total Ag2School Credit Percent |

| 2021 | 5% | 55% |

| 2022 | 5% | 60% |

| 2023 | 10% | 70% |

It would take action in both the House and Senate and a signature by the governor to not have these scheduled increases take place.

“Repealing or reducing the program would mean a vote for raising taxes on the backs of rural Minnesota farmers and harming equity in school funding for kids and parents,” said Sam Walseth, MREA Director of Legislative Affairs. “Not only is this extremely unlikely, but the strong coalition of like-minded rural interests (MREA, farm groups and others) would link arms to defeat any attempt to renege on the Ag2School credit to farmers for school facilities for rural children’s education.”

Prior to an increased credit going into effect, it is possible that legislators could delay, modify or eliminate future scheduled credit increases without “raising taxes.” The next budget-setting Legislature is in 2021 and if the state’s budget is in poor shape, lawmakers could affect the scheduled credit increases for Pay ’22 and ’23.

Given the growing uncertainty and risks built into the state budget, the credit increases above 55% in Ag2School could be vulnerable to modification. MREA and many others will continue to advocate to keep the scheduled increases in place. However, this is the one cautionary note in an otherwise outstanding development for farmers and rural schools.

Next Steps

Financial decisions are never easy, especially when considering asking voters for approval of a bond or operating referendum. These take the assistance of financial advisors. If your school district does not have a relationship with a financial advisor, see a list of financial advisors.